The 2026 London Private Aviation Report: Trends, Destinations and the Future of Charter

- Feb 24

- 8 min read

Updated: Feb 26

London's private aviation sector continues to evolve at a remarkable pace. As we move through 2026, the industry is experiencing a fundamental shift, not just in where clients are flying, but in who is making those bookings, what they're bringing along, and how they expect their charter experience to be structured.

Drawing on recent flight data, industry observations and insights from our own booking patterns, this report examines the defining trends shaping London's private aviation landscape in 2026.

The PA Effect: 65% of Bookings now managed by Executive Assistants

Perhaps the most significant shift in private aviation booking behaviour is the rise of the Personal Assistant and Executive Office as the primary point of contact. Our data indicates that approximately 65% of private jet charters originating from London are now arranged by PAs, family office staff, or corporate travel coordinators rather than directly by the principal traveller.

This trend has profound implications for how charter services need to operate. PAs require a different level of communication - they juggle multiple priorities, coordinate complex itineraries and often manage last-minute changes on behalf of demanding principals. They need clear pricing structures, responsive 24/7 support and straightforward documentation.

The most successful charter relationships in 2026 are built on trust and education. Many PAs are booking their first private charter and need guidance on everything from aircraft selection to customs procedures. Recognising this shift, our PA training programmes have seen a 40% year-on-year increase in uptake, with assistants seeking to understand baggage allowances, pet policies, catering timelines and the nuances between aircraft categories.

When a PA knows they can rely on transparent pricing, guaranteed hourly rates and protected funds held in trust accounts, it removes the uncertainty that can make private aviation feel opaque or risky. This level of structural reassurance is becoming a baseline expectation rather than a premium feature.

Top Destinations from London: Where are We Flying in 2026?

London's position as Europe's premier private aviation hub remains unchallenged. With utilisation rates at London Biggin Hill and across the broader London airport network exceeding pre-pandemic levels, the capital serves as the departure point for a consistent set of high-frequency European sectors.

Based on charter activity from the last 6 months, the destinations we are repeatedly seeing at the top of the list are:

Nice Côte d'Azur (LFMN) – Still the anchor route for leisure and mixed-purpose travel, with summer inventory often feeling “spoken for” earlier each year.

Málaga (LEMG) – A strong all-season performer for Costa del Sol leisure, property visits and quick corporate trips where your schedule does not tolerate airline connections.

Faro (LPFR) – The Algarve remains a dependable favourite for golf, family travel (often with pets) and short-notice weekend sectors.

Geneva (LSGG) – A year-round business gateway that also absorbs winter leisure demand, particularly for alpine access where timing matters.

What's notable is the increasing deployment of Super Light and Light aircraft on these routes, delivering the right balance of cabin comfort and operating economics on 1.5 to 2.5 hour sectors, particularly when you are prioritising departure time certainty and airport proximity.

The Pet Flight Boom: A 20% Year-on-Year Increase

One of the more charming trends we've observed is the dramatic rise in pet-accompanied flights. Bookings explicitly requesting pet-friendly aircraft configurations have increased by 20% compared to the same period in 2025.

This isn't merely about allowing your 4 legged friend in the cabin, it reflects a broader lifestyle shift. With more clients working remotely from second homes in Europe, pets are becoming permanent travel companions rather than occasional passengers.

Aircraft operators are responding accordingly, with more airlines increasing their choice of airports permitted to enter the UK, such as Oxford, Biggin Hill or Farnborough. On present trends, we think this will continue to rise.

Market Dynamics: Growth, Sustainability, and Regulatory Adaptation

Recent flight data from mid-February 2026 showed 977 private jet movements in the UK during week seven: a 32% increase week-on-week, though down 4% year-on-year. This pattern reflects the sector's maturation - rapid week-to-week variability based on events, weather, and school holidays, but steadier long-term growth trajectories.

Globally, the private aviation market is projected to expand at a 6.7% CAGR through 2030, driven by increasing corporate adoption, fragmented commercial airline schedules and growing wealth in emerging markets.

However, the industry is simultaneously navigating intensifying sustainability pressures. European operators, including those serving London, are retrofitting fleets with sustainable aviation fuel (SAF)-compatible engines to comply with ReFuelEU carbon thresholds. While SAF currently represents a small fraction of total fuel usage, regulatory mandates are accelerating adoption.

For clients, this means gradual price adjustments as operators absorb retrofitting costs and SAF surcharges. Transparent brokers are already building these considerations into long-term pricing models rather than introducing surprise levies mid-contract.

The France Solidarity Tax: Why it matters most on Light and Super Light Aircraft

If you are planning sectors into France in 2026, it is worth being aware of the new per-person “solidarity” style tax being applied on qualifying departures/arrivals, because it tends to be felt far more sharply on smaller-cabin categories.

Where this becomes material is the arithmetic: a fixed charge per passenger does not scale with the aircraft’s hourly cost. So, when you are travelling on a Light or Super Light Jet, the tax can represent a meaningful percentage uplift to the total trip cost; whereas on a larger Super Midsize or Ultra Long Range aircraft, it is typically diluted across a higher baseline operating cost (and, in many cases, more seats).

If you need pricing certainty for France-heavy flying, this is precisely where a structure such as our Protected Hourly Rate programme can be helpful, because you can plan with a clear ceiling cost per hour while still benefiting from real-time market pricing underneath, rather than being exposed to drift as fees evolve around peak dates.

UK Domestic Travel: Cabotage constraints, fewer Options, and a shift to Helicopters

UK domestic private aviation has also become more complex. Cabotage restrictions have reduced the pool of operators that can legally perform certain UK-only sequences, which on occasion means fewer aircraft options and higher pricing, particularly where an operator must position in an eligible aircraft and crew, or where the routing cannot be optimised in the way it would be on a cross-border itinerary.

In practice, this has shown up as:

Premiums on Friday/Sunday domestic legs, especially when the aircraft needs to “dead-leg” to stay compliant.

More limited last-minute availability, even when the overall market looks healthy on paper.

The market is compensating in two ways. First, we are seeing new operators and additional lift entering to serve the gaps. Secondly, there has been a clear rise in helicopter charters for UK domestic hops where timing, access and point-to-point practicality outweigh the traditional jet solution (particularly for city-to-estate, event-day moves, and multi-stop days).

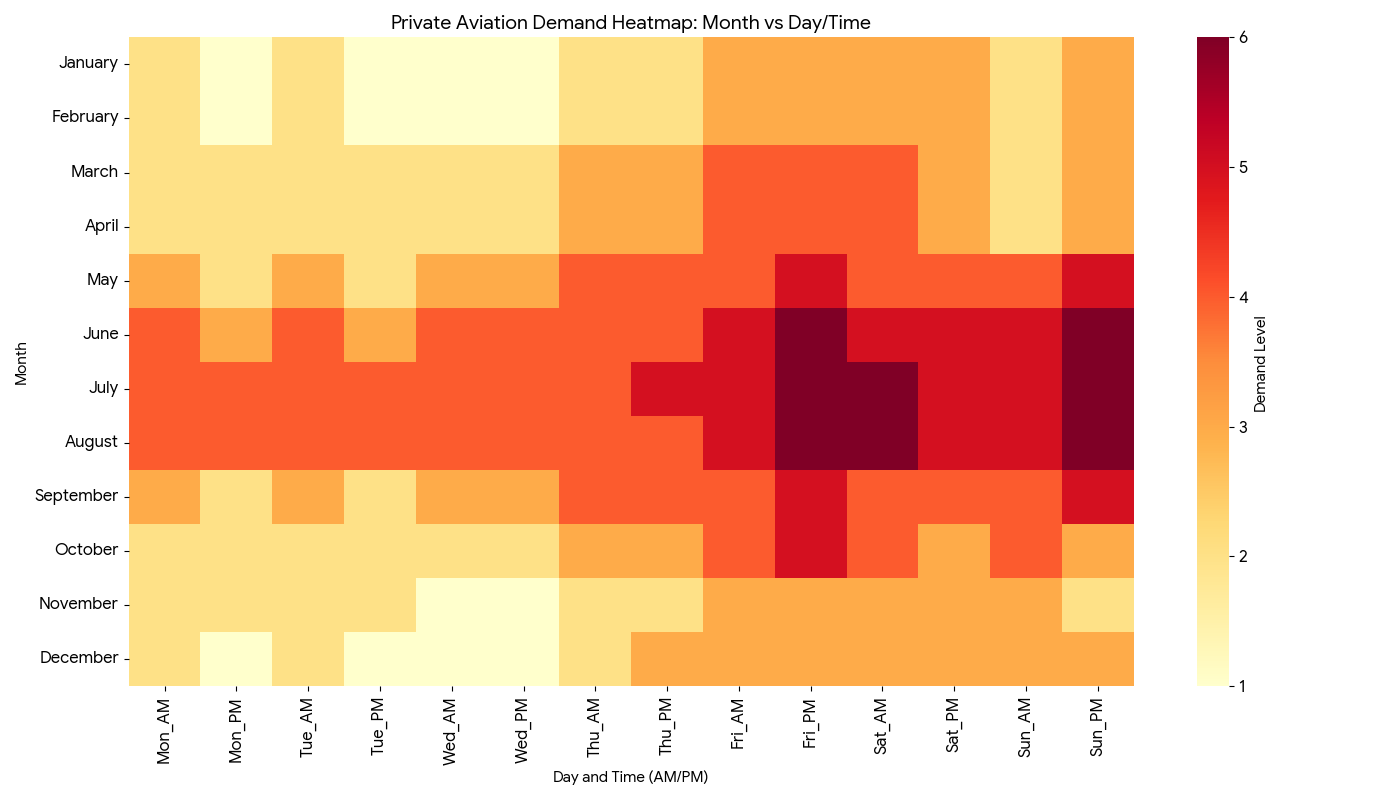

Scheduling Reality: Why Tuesday/Wednesday can be the Sweet Spot

If you have flexibility, the simplest lever to pull in 2026 is often the calendar. Demand is peaking over weekends, which means the best availability (and often the cleanest pricing) is typically found on Tuesdays and Wednesdays. When you look at the heatmap below, you can see the concentration of demand building towards Friday and remaining elevated through Sunday, which is typically when availability tightens and the market introduces premiums.

When you can travel midweek, you may also reduce the risk of having to accept sub-optimal aircraft choices simply because “everything is already out” on the Friday/Sunday wave.

The Midsize Gap: Fewer obvious “Step-up” Options, and a Split in Buyer Behaviour

A quieter but important change is what has happened to the traditional midsize “workhorses”. Clients who historically flew aircraft such as a Hawker 900 or Learjet 60 are finding there are now fewer straightforward choices, and that Midsize pricing can land uncomfortably close to Super Midsize on many European city pairs, particularly during peak windows.

This has increasingly split demand into two practical pools:

Pool A: VLJ through Super Light (where the aim is to control total trip cost while still improving on airline timing and privacy).

Pool B: Super-midsize and larger (where the aim is to protect cabin comfort, baggage volume and operational resilience, even if the hourly rate is higher).

This is also where your pricing protections matter. If you are comparing categories that are converging in price, having access to real-time market pricing with a protected ceiling can alleviate the uncertainty that tends to appear right before departure, particularly around weekends and event-driven peaks.

Citation Ascend: Arrival in Europe, and a Cabin Height Question to Watch

The Citation Ascend is now beginning to appear more regularly in European charter conversations, and it is naturally being cross-shopped against the established Citation XLS (560XL series) family.

One point worth noting, if cabin comfort is a deciding factor, is that there is some concern in the market that the Ascend’s flat-floor approach may come with a trade-off, namely, reduced central cabin height compared to what frequent XLS flyers are used to. For some travellers, that may be irrelevant; for others (particularly taller passengers, or those who spend time moving around the cabin), it can influence whether the aircraft “feels” like a comfortable step-up or simply a different layout.

If you are booking for a principal who is particular about cabin geometry, it is sensible to request precise cabin dimension sheets and, where possible, comparable interior photography of the exact tail being offered.

Looking Ahead: The Future of London Private Aviation

As London retains its status as Europe's leading private aviation hub, the sector is maturing from a luxury novelty into a sophisticated business tool. The rise of PA-led bookings, pet-inclusive travel, and demand for pricing transparency all point toward a more professionalised, client-centric industry.

For those new to private aviation, whether you're a PA booking your first charter or a Corporate Travel Manager evaluating options, the key is to work with brokers who prioritise education, protection and operational clarity over sales pressure.

The London market will continue to grow, routes will evolve, and sustainability will increasingly shape aircraft selection. But the fundamentals remain unchanged: transparent pricing, rigorous safety standards and genuinely responsive service are what separate exceptional charter experiences from merely adequate ones.

The Jet Members Difference: Protected Rates, Quality-First Standards

In an industry where price opacity and last-minute surcharges have historically been pain points, structural protections are becoming essential, particularly for PAs managing executive travel budgets.

Protected Hourly Rate programmes provide certainty of cost without committing you to a fixed hourly rate each time, which can be helpful if you want to know how much 25 hours will cost (as a maximum fee) without being committed to paying that same rate on every trip.

Your choice of aircraft should never compromise on safety standards, regardless of budget. Quality and reliability at the aircraft level also include avoiding aircraft manufactured before 2004. In practical terms, that typically means you are less exposed to the compromises that can come with older airframes and legacy interiors, and you are more likely to see consistent cabin finish, connectivity expectations, and operational dependability across your flying.

And if things do go wrong (because aviation is still aviation), members also benefit from Aircraft On Ground (AOG) protection, designed to ensure you are not left stranded if a booked aircraft becomes unserviceable close to departure; we will source suitable replacement lift as quickly as operationally possible, keeping your schedule protected.

Jet Members - Building Tailored Programs for Clients

Searching for the right membership discreetly, if you would like to explore what that could look like for your travel pattern, we have an easy-to-follow guide to exploring our membership plans.

With more demand expected in 2026, tailored flying packages are becoming more popular, with the freedom to choose specific aircraft without long-term obligations or risk of expiry.

Comments